So you’ve been traveling more and more in your RV and are now seriously thinking of going full time. I know it can be exciting but also nerve-wracking, what with all the changes that you have to plan and prepare for. Among the many things that need adjusting like logistics and living conditions, RV insurance should be high above your list. Let me walk you through the things that you must consider when getting full-time RV insurance.

What is a full-time RV insurance? Most full-time RV insurance includes coverage on the RV, damage to belongings, and personal liability, similar to a homeowner’s insurance. Riders can be added for better coverage like roadside assistance, uninsured motorists, and emergency expenses.

Navigating the world of RV insurance can be dizzying but worry not. In the following sections, I’ll tell you the benefits of getting full-time insurance, how much it costs, and the common pitfalls that you want to avoid when getting one.

Why You Must Insure Your RV

An RV, whether brand new or pre-loved, is an expensive purchase. It’s not just a car, it’s like a mini home. And just like our homes (or even our cars for that matter), we like to take good care of them and keep them in tip-top shape. Maintenance can be anything from small scratches to big bumps to failing machinery inside the RV. All these fixes may not cost that much individually but add them all up and you’ll see how it can take a considerable chunk from your pocket. An insurance policy can help you by shouldering these expenses instead of taking it from your savings.

Having coverage for motorhomes is also required in most states and for good reason. They are big, powerful vehicles that can cause serious and costly damage. Imagine where you’ll get the money if you got in an accident and your RV got totaled, or anyone involved needed medical care, or someone sues you for damages. Many things can go wrong and you want to be insured for that.

Now, if you’re planning to get a loan from the bank or other lending companies to finance your RV, many will require you to have insurance first. They have to protect their money too! In case something happens to the vehicle before you’re even done paying for it, it’s good to have enough coverage to take care of what you still owe instead of finding yourself in serious debt.

Full-Time RV vs Part-Time RV vs Auto Insurance

Let me just put it out there that having auto insurance doesn’t cover your RV. First, the cost of maintenance is higher for RVs. Second, the damages that a car can cause is significantly smaller than your motorhome. So do not automatically assume that auto insurance is good enough.

Having that out of the way, I know you want to know what your options are to make sure that your RV is covered. Here are the two main choices that you can consider.

Part-Time or Storage Coverage

Part-time insurance is good for anyone that uses a mobile home for less than half a year. If you’re a weekend or occasional camper, you might want to give this option a look. Having this kind of policy insures your RV for any damages while in storage. This includes vandalism, damages due to forces of nature like storms or tornadoes, and accidents like storage fires.

It is important to note that part-time insurance covers only your RV during its storage time. It’s a whole new game when you decide to hit the road. Medical, liability, and legal expenses are outside the protection of your policy once you’re out there.

For this reason, it is advisable to call your agent prior to traveling to switch to full-time insurance. Let them know when you plan to leave and come back home. Full-time insurance gives you more liability and protection coverage than part-time insurance. You can always switch back to part-time once you get safely home. This way you don’t have to pay a full-time premium while your RV is in storage.

Some part-timers opt for campsite liability instead of going full-time all the way. This includes many benefits of full-time insurance like medical expenses of people loitering around the RV. If you don’t wanna shell out a lot for full-time insurance, this could be a good choice for you.

Full-Time RV Insurance

Full-time RV insurance is much like a homeowner’s insurance. It covers not just your motorhome but also your personal liability and your belongings. Medical expenses, accident coverage, maintenance, and more benefits are included in full-time insurance. We’ll talk more about these in the next section.

When to Consider Part-Time RV Insurance

If you’re more of a hobbyist and find yourself a lot more at home than on the road, part-time insurance might be your best choice. Have this coverage when your RV spends more time in storage, like more than half a year.

Some companies will ask you upfront how often in a year you plan to take your baby out driving and adjust the bill based on it. Others will require you to inform them whenever you’d take out the RV. Ask your agent about the company’s rules to have sure full coverage while traveling and less payments while your van is in storage. This will save you some bucks instead of paying full-time the whole year for something that you use for only a couple of weeks.

When To Consider Full-Time RV Insurance

A rule of thumb is if you’re on the road, get full-time insurance. Whether the RV is your own or if you’re renting one, having the van and yourself covered is always a good idea. Remember that this is like your home. Whether owned or rented, damages will have to be paid.

And this is regardless of where you are in the country. Before going YOLO (you only live once), check state and cross-border rules about insurance. Each state has a different requirement and you better be prepared to avoid surprises while traveling. But one thing is for sure– they all require you to get insurance.

If you’re paying for your RV via bank or lender loans, be insured to protect yourself from future debt. Some banks do not require the policy to cover the whole cost but this can backfire if something happens to the van. You’ll still have to pay for the remaining balance and we know that RVs are not cheap. Do yourself a favor and get insurance that covers the full price of your RV.

Benefits of Full-time RV Insurance

Core Benefits

The basic idea with full-time RV insurance is that you’ll be trying to replace your home and your belongings in case of unforeseen events. It is good to cover as much as you can to protect yourself from the possible loss of home and property.

Property Insurance

The main benefit of full-time RV insurance is coverage for the RV itself. Your policy should be able to cover a reasonable amount for fixing damages to your van. More importantly, it should cover the cost of replacing your van in case it got totaled in an accident.

Remember to get coverage for replacement cost instead of for actual cash value or ACV. Replacement cost will give you the amount needed to actually replace your unit. ACV will cover only the agreed value of the RV upfront based on third-party sources. For example, if you bought your RV at $100,000 and took it out of the dealership, it would automatically depreciate in value. If you get the policy after buying it, that depreciated value has a good chance to be the sum covered in ACV.

Personal Liability

Full-time coverage will protect you from expenses due to accidents in or around your property. If the neighbor’s kid trips on one of your lines or one of your friends parties too hard in your RV, they can both file for claims. Your policy will cover these claims for you.

Medical Expenses

Aside from the day-to-day small accidents, your RV’s insurance will pay for any medical expenses incurred even in big accidents. Whether it’s for your care or for another motorist, having protection from medical bills is always a plus.

Personal Belongings

Since you will be treating your RV as your home, you’ll probably take your valuables with you. In case of a collision and your expensive stuff goes flying around, insuring your personal belongings will enable you to replace them without having to pay for them out of pocket.

This value can be adjusted based on your needs. If you own pricey things like laptops, cameras, and other expensive equipment, get the sum of all these and go a bit higher. Some motorhome owners go even twice or thrice the current price of their stuff. Of course, they’ll need to pay more for something that they may never use ever but this is a balancing act that every RVer needs to do for themselves.

Riders

Additional protection comes in handy for special cases like roadside trouble. The main thing is to ask your agent if these are included. If not, you can request to have them added to your plan. Take a look at some of the popular riders that you can include in your RV insurance.

Towing and Roadside Assistance

In case of a breakdown in the middle of nowhere, you can call for assistance to replace tires, fluids, and batteries. Some companies will tow your RV to the nearest shop if it can’t be fixed on the road.

Emergency Expenses

A roadside breakdown can render your RV unusable for several hours or days. If this is your home, where will you live? This rider will cover your expenses for food and lodging in the event that you can’t use your RV. It usually requires the breakdown to be a certain distance from your home so you need to take note of that.

Uninsured or Underinsured Motorists

You may be a careful driver, but accidents can still happen, and it may involve another driver that may not have enough insurance or none at all. One or both of you could get hurt. He may sue. He may not be able to pay for damages if the accident was his fault. The uninsured motorist rider can help you cover damages and expenses incurred in such scenarios.

Cross-Border Insurance

As free as it sounds, you can’t just go traipsing around and outside the country expecting to be insured. Most insurance will tell you where the coverage ends and you should be mindful of that. If you plan to go somewhere your policy does not cover, talk to your agent to discuss if cross-border insurance can be added to your plan.

How Much RV Insurance Costs

All that benefit sounds fantastic but not everyone is crazy about the price. Put your judgment on hold and check out the factors that determine the premium and the common price range of full-time RV insurance.

Factors Affecting Cost

Class of RV

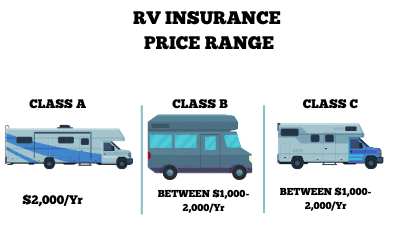

RVs are classified into three main classes. Class A is for luxury couches and convertible buses. It can fit an average of 8 people inside and can usually be seen used by celebrities. Think super expensive and that’s class A. And more expensive RVs will require higher premiums.

Class B are your trailers and camper vans. They tend to be smaller than classes A and C but they still have the basics like a kitchen, beds, and bathroom. This is great for people that plan to spend more time outside the RV itself. It’s also more fuel-efficient.

Class C uses the cargo van as the driving part. They fall between classes A and B in size and price. They provide the comforts of class A, just a little toned down while staying near the price point of class B.

RV Age and Condition

If you decide to get insurance in the middle of your RV’s life, your motorhome will have already seen some action. In this case, the company will assess the value of your RV and how well it was taken care of. This will determine how much they’ll be willing to cover for your van.

Frequency of Use

As mentioned previously, you need to inform your agent of how often you intend to use the RV. Will you use it all year round, monthly, holidays? This will enable them to give good advice on the coverage you need.

Driving, Claims, and Accident Records

Higher risks mean higher premiums. Insurance companies will be sure to ask about your driving history before committing to anything. Any previous claims and incidents, whether it’s your fault or not, will play a role in their approval and the limits that they will allow for your policy.

Policy Limits

You can request for higher coverage in any part of your policy but it will come with a price. Whether it’s to comply with state requirements, loan requirements, or just personal preference, you will pay a proportional amount of premium to increase your protection.

Price Range

If you’re wondering how much RV insurance actually costs, full-time coverage for class A van is $2,000 or more per year in 2020. Class B costs between $1,000-2,000, and class C falls somewhere in between.

A full-time RV couple earlier in the year had part-time insurance at $1,200 per year with $10,000-20,000 limits in coverage. After an acquaintance who is an agent pointed out how unprotected they were, they later decided to shift to full-time insurance at the price of $1,649 per year with $100,000-300,000 limits. That’s a premium difference of approximately $450 per year for way better coverage.

Check If You Qualify for Discounts

Any savings are welcome and you should check with your agent if you qualify for any promos. Some companies offer cheaper multi-vehicle insurance for when you have an RV and a separate car. Some even give discounts to owners that have clean driving records and have had no claims in the past where they were found at fault. Note also that paying your premium in full instead of installments can lower your payment.

Full-time Insurance Might Seem Expensive But…

Try looking at it this way; If you get in an accident, where will you get the money to pay for medical bills, fix your RV, and pay for legal claims? Policy premiums definitely cost less compared to the damages that you’ll need to worry about in case of emergency.

Common RV Insurance Mistakes

You can never know too much when it comes to RV insurance. It’s always safe to just ask and research if you’re unsure about something. To give you an idea about what to ask, take a look at some of the common mistakes when getting RV insurance.

Assuming Your Belongings Are Insured

Many policies will not include your belongings in the insurance policy. This is a separate clause and you need to check if they are part of the coverage, especially if you have expensive stuff that you’ll need to replace.

Getting Insurance In Haste

Buying a big-ticket item and getting an insurance policy for said item is stressful. Pressure can rise if you’re very eager to get the purchase over with, which can cause you to settle with whatever insurance you can get. Set aside time to think it thoroughly. Your future self will thank you for it.

Not Telling The Company That You’re Full Time

As mentioned a couple of times in previous sections, let your company or agent know how often you intend to use the RV. If you just decide to go on the road and something happens, the company may reject your claim. Telling them about your plans will also allow them to give you advice if you have enough protection.

Not Getting Commercial Policy

Earning profit from any business in your RV will require you to disclose that you’re using the van for commercial purposes. I know it may sound a bit too much but even a dollar earned in your RV by filming YouTube videos can be considered commercial. If you’re using the RV for business trips, holding meetings, or any business-related functions, be sure to let your agent know.

Not Updating The Policy Once Transitioned To Full Time

Many motorhome owners start out as part-timers that eventually shift to full time. Most of the time they will get part-time insurance and forget to update their policy once they make the shift. This leaves many vulnerable thinking that they’re fully covered. Remember to add this task to your checklist when transitioning.

Overweight content

RVs come with specifications from manufacturers about the weight it can hold and you should mind it. Don’t worry, they won’t weigh you, just your belongings. The insurance company can deny claims on the basis of overweight content if there are any accidents. Stay within your van’s limits and you’re good to go.

Reminders When Considering RV Insurance

Be it part-time or full-time RV insurance, binge on articles, videos, and any advice you can get from companies and other owners. With so many nuances in RV insurance, one can easily get lost in the sea of options. Consider your personal needs and imagine possible scenarios that will need coverage.

And get a good agent! Have one that you trust will lead you to the best policy for your needs. Don’t be afraid to ask questions. Lots of questions. Specific questions. If you are not satisfied with your agent or company, find another one. They should explain things to your satisfaction because this is a pretty big investment.

Conclusion

Turning full time as an RV owner is a big change that comes with important things to consider. Just like any change you want to minimize the risks and be as prepared as possible. Give serious thought about protecting yourself and your property for unforeseen events, and enjoy peace of mind as you drive to your next destination.